Empowering Growth, Shaping the Future.

Dubai Investments has built a strong UAE presence across key sectors through innovation and sustainability.

.gif)

Dubai Investments has built a strong UAE presence across key sectors through innovation and sustainability.

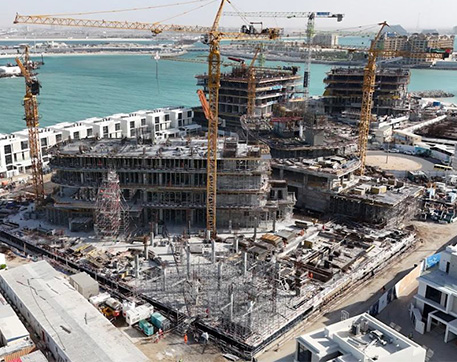

Dubai Investments Breaks Ground on Landmark Al Vista Mixed Use Development in Meydan

Subsidiaries, Associate Companies & Joint Ventures

Total Assets

(As of Dec 31 2025)

At Dubai Investments, we are proud to serve as a catalyst for economic growth, embodying stability and innovation while contributing significantly to the UAE’s diversification strategies.

Our Mission is to add value and expand DI’s investment portfolio through sound corporate citizenship, financial engineering, network of relationships, and financial resources.

Our vision is to provide impeccable quality by delivering superior management performance and top of the line services to our investors. An integral part of this vision is delivering superior returns to our shareholders, consistent with our pre-defined risk profile and comparable to other best-in-class corporations. We strive to increase the value of our business while maintaining high ethical values and a commitment to the development of society through integrity and fair business practices.

ESG Report 2024

Dubai Investments warns all investors to verify the identity of the entity they are dealing with before signing any agreements or making any financial transactions, and to refer to Data related to licensed companies published on the Dubai Financial Market’s website in order to avoid exposure to any fraudulent operations by unknown entities.

✓ Success